IGS Energy Market Insights: A Bull Market for Natural Gas

In recent weeks, a nearly 7-year cap on energy prices has quickly vanished, leaving many businesses contemplating the right next step to hedge against a volatile natural gas market. But while there are several indications prices will continue to rise, there's an opportunity to lock in more affordable gas rates this season.

What businesses should know about the natural gas market

In recent weeks, a nearly 7-year cap on energy prices has quickly vanished, leaving many businesses contemplating the right next step to hedge against a volatile natural gas market.

But while there are several indications that natural gas prices are going to continue to rise, there is also an opportunity to lock in more affordable gas rates this season.

For customers willing to consider a fixed long-term natural gas strategy, long-term prices are still affordable. (Notably, winter 2023-2024 and winter 2024-2025 should be considered.)

In this article, we highlight natural gas production and export trends, the market indicators driving recent price increases and the status of natural gas storage – as well as what actions businesses can take to protect themselves from rising prices.

Changes in U.S. natural gas production and export growth

When examining what's driving the price of natural gas, there are two main things to look at: U.S. production and exports.

At the start of 2017, the U.S. was producing 70 billion cubic feet (Bcf) of natural gas every day. (Bcf is the standard unit of measurement for natural gas supply and demand; 1,00,000 MMBtu = 1 Bcf.) Over the next few years, production increased significantly – by 25 Bcf a day – driving the price down while fueling increased exports: From 2016 to 2021, liquefied natural gas (LNG) exports increased from 0 to 11 Bcf a day.

So, where are we today?

After large increases in production since 2017, producers in 2021 hit the pause button. Supply has remained a constant 91 Bcf a day, while demand has continued to increase.

When looking at U.S. net supply, which is production plus imports minus exports, we've averaged around 78 Bcf a day to meet gas demand within the U.S. Five years ago, U.S. net supply averaged 74 Bcf a day – just 4 Bcf a day higher. And in the last five years, a lot has changed on the demand side:

- The U.S. has retired many coal and nuclear power plants, leaving a gap in the power stack that's primarily filled by natural gas (though renewable energy generation has increased).

- At the same time, industrial production is driving demand higher.

- Natural gas producers, meanwhile, are not increasing production, but are sticking to their plans to reduce capital expenditures and debt.

This, along with tremendous increases in global energy prices, has resulted in the recent increase in the price of natural gas.

Natural gas market indicators

Here's a brief summary of the indicators currently driving the natural gas market:

Bullish:

- An increase in natural gas exports

- Constrained production of natural gas in the Northeast

- An increase in industrial demand for natural gas

- Storage levels below the 5-year average

- Political desire to reduce carbon fuels

- Reluctance from producers to increase supply

Bearish:

- Renewable power buildout

- The potential impact of climate change and warmer winter weather

- States limiting natural gas (notably New York and California)

- An increase in drilling if prices become favorable

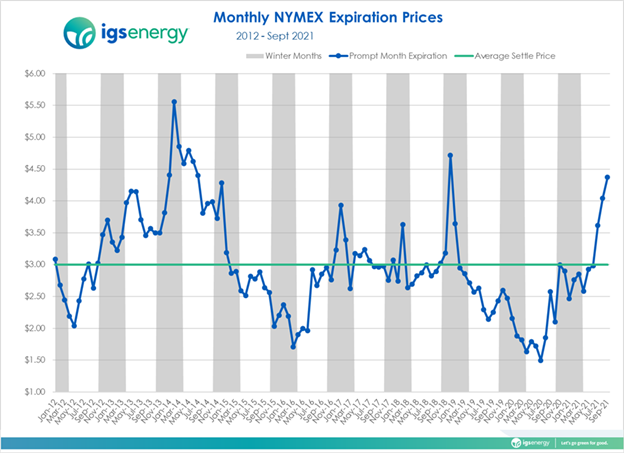

U.S. natural gas prices: a bull market for natural gas

From April 6 to September 9, natural gas prices doubled, going from $2.45 to over $5.00. Recently, prices shot up over $6.00 before falling back to $5.00.

The last time we experienced a prompt-month contract higher than $5.00 was during the winter of 2013-2014 – when we were experiencing the eighth-coldest winter in the last 71 years. In November 2018, we again experienced a price run-up, due to a very cold start to winter (the ninth-coldest November in the last 71 years).

What's striking about what we've seen recently is that the price of natural gas spiked in the summer.

Because natural gas is a winter commodity, prompt-month run-ups historically occur during a winter month. When we experience cooler-than-normal temperatures, prices increase and, when cooler temperatures hit early in the season, the odds will tell you to protect the balance of the winter by increasing the price. The recent run over $5.00 is unusual in that it happened in September – not historically a high-price month.

As we turn our focus to winter prices, January 2022 was north of $5.40 (as of mid-September).

{kind=link}

Natural gas storage concerns: lower inventories predicted this winter

The Energy Information Administration projects U.S. inventories of natural gas will reach 3.592 trillion cubic feet (Tcf) by November 1, the beginning of the winter heating season. This is 159 Bcf below the earlier five-year average.

This past winter, the U.S. withdrew roughly 2.2. Tcf of natural gas from storage – taking us from 3.95 to 1.75 Tcf. Based on the EIA figures, we can expect to inject 1.85 Tcf this summer, which is well below what the U.S. withdrew from storage last winter, suggesting that demand for natural gas is outpacing supply.

A couple things to note:

- Last winter was not exceptionally cold. The extreme weather in Texas remains the event we remember most from last winter but, from November 2020 to March 2021, the winter was much warmer than both the 10- and 30-year average. In fact, last winter was the seventh warmest in the last 71 years. We don’t need a cold winter to stress the gas system.

- With just a few weeks left in injection season, we’re not likely to reach the 3.7 Tcf we need to achieve a comfortable storage level.

With natural gas prices currently much higher than the 5-year average for the summer, we’d expect to see an increase in storage injections, as higher prices tend to attract production. But higher prices do not seem to be influencing production.

Low storage paired with increased exports and high demand indicates the likelihood of high gas prices is not likely to diminish anytime soon.

How businesses can protect themselves from price volatility

Natural gas prices aren't likely to dip below $2.00 – though they are very likely to continue to increase above $5.00.

The good news: Long-term energy prices are still affordable and should be considered carefully by energy buyers. As of October 15th, the winter is currently trading around $5.50:

- Winter 2023-2024 is trading around $3.65

- Winter 2024-2025 is trading around $3.45

Considering the increasingly global demand for natural gas, there’s an incredible opportunity now for energy buyers to lock in long term at the lower prices.